Chimp Change

Chimp Change

Turning Small Savings into Big Returns with Compounding

Compound interest is the eighth wonder of the world. Those who understand it, earn it; Those who don’t, pay it.

Albert Einstein

Compounding. We hear this word all the time, and may even use it on a daily basis, but do we really understand what it means? This post will dive into compounding and why you should care about it.

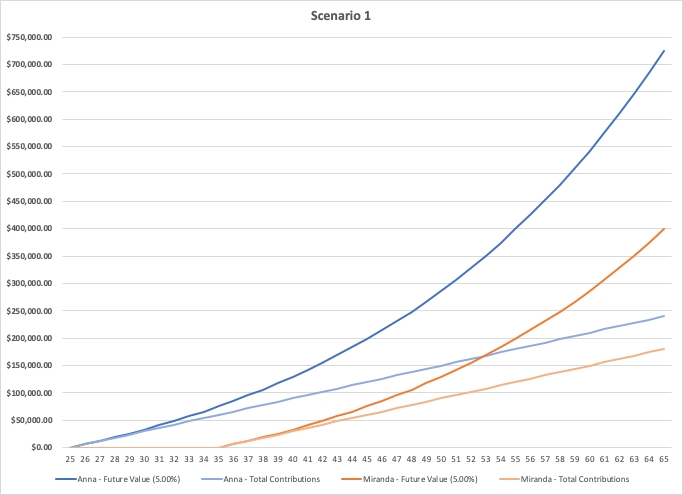

Take Anna, for example. Anna just graduated from college at the age of 25. She soon after started working at a company which paid her enough to have an extra $6,000 after considering all of her expenses each year. She made the financially literate decision to save the $6,000 dollars in a savings account for when she would retire at the age of 65. Miranda also started working at the age of 25 and saw that each year she had an extra $6,000. Miranda, however, decided that she didn’t feel the need to start saving while she was this young. Miranda started saving $6,000 a year for retirement when she turned 35 and also planned to retire by the age of 65. By retirement, Anna had deposited $240,000 and Miranda had deposited $180,000 into their respective savings accounts. Both of their accounts had an interest rate of 5%. However, when both women opened up their savings accounts, they were shocked at the difference in savings. Anna had saved $724,798 and Miranda had saved $398,633. While only differing in $60,000 of initial deposits, they saw a difference of $326,165 in their savings at retirement.

You probably think I’ve messed up with my calculations somewhere but I assure you I have not! What you have seen is the magic of compounding occurring before your very own eyes. The reason Anna and Miranda saw such a difference in their savings is due to the magic of compounding!

The term compounding, or compound, means to combine or in this case, add on. The first $6,000 deposited gave each account $300 in interest. This means, by the time the first year of saving is completed, both Anna and Miranda have $6,300 in their savings account. Now this is where compounding comes into play, with the next yearly deposit of $6,000; both women have $12,300 in their savings account, with a 5% interest rate. Both accounts had $615 of interest added to them. With more and more money being deposited into the account, the 5% yearly interest increases.

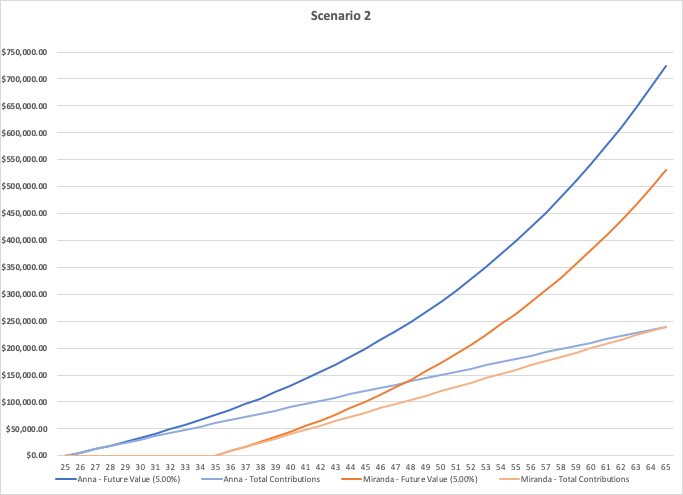

Let’s consider another scenario. Assume that Anna saved the same amount over the same period of time, giving her $724,798 in her savings account by the age of 65. However, let’s assume that Miranda would instead deposit $8,000 yearly, from the ages of 35 to 65. By the age of 65, both women would have deposited $240,000 by retirement. However, Miranda would only have saved $530,979, in comparison to Anna’s $724,798. Even though both Anna and Miranda deposited the same amount of money, there was still a $193,819 difference in savings.

This brings us to the main way to maximize compounding: time. The only difference between Anna and Miranda in the second scenario was how long they had been depositing in their savings account. The longer you allow your money to compound, the larger the yearly interest will be. Even if your deposits are not as large as Anna and Miranda’s, over time your deposits will grow exponentially.

Even after taking a quick look at all the graphs, you can clearly see how in the last couple of years, the money increased far more quickly. Time is your biggest asset when it comes to saving.

If Miranda had been shown the benefits of compounding (just like how I’m showing you), she probably would have thought twice about waiting to open a savings account 10 years into her working career. She would have started saving earlier to gain larger benefits from compounding.

My dear Money Monkeys, the one main idea I wish for you to take away from this post is, don’t be like Miranda. Instead, understand the benefits of compounding and make the informed decision to start saving as soon as possible!

Next time we shall cover budgeting and how to save, to allow yourselves to have money to deposit into a savings account. Don’t worry, compounding will make a return when we talk about investing!